Table of Content

Some home buyers hold credit scores over 800 and can’t get approved, and others have credit scores of 500 and buy their first home in 30 days. After the Great Recession of 2009, subscription-based credit companies emerged to help consumers build good credit. One credit builder, StellarFi, will automatically pay your bills to build your credit. Then payments are directly reported to Experian®, TransUnion®, and Equifax®, to quickly build a positive payment history for its members. Resist the urge to close the old credit cards you never seem to use; and, the personal charge card for the store you never visit.

It’s never too early to get started, and it sometimes can be too late. Check your buying power by getting pre-qualified for a mortgage with us at Zillow Home Loans. Andrew Dehan is a professional writer who writes about real estate and homeownership. Alt-A is a classification of mortgages with a risk profile falling between prime and subprime. The lender will want you to pay off any outstanding collections and judgments.

HOMESTAR Blog

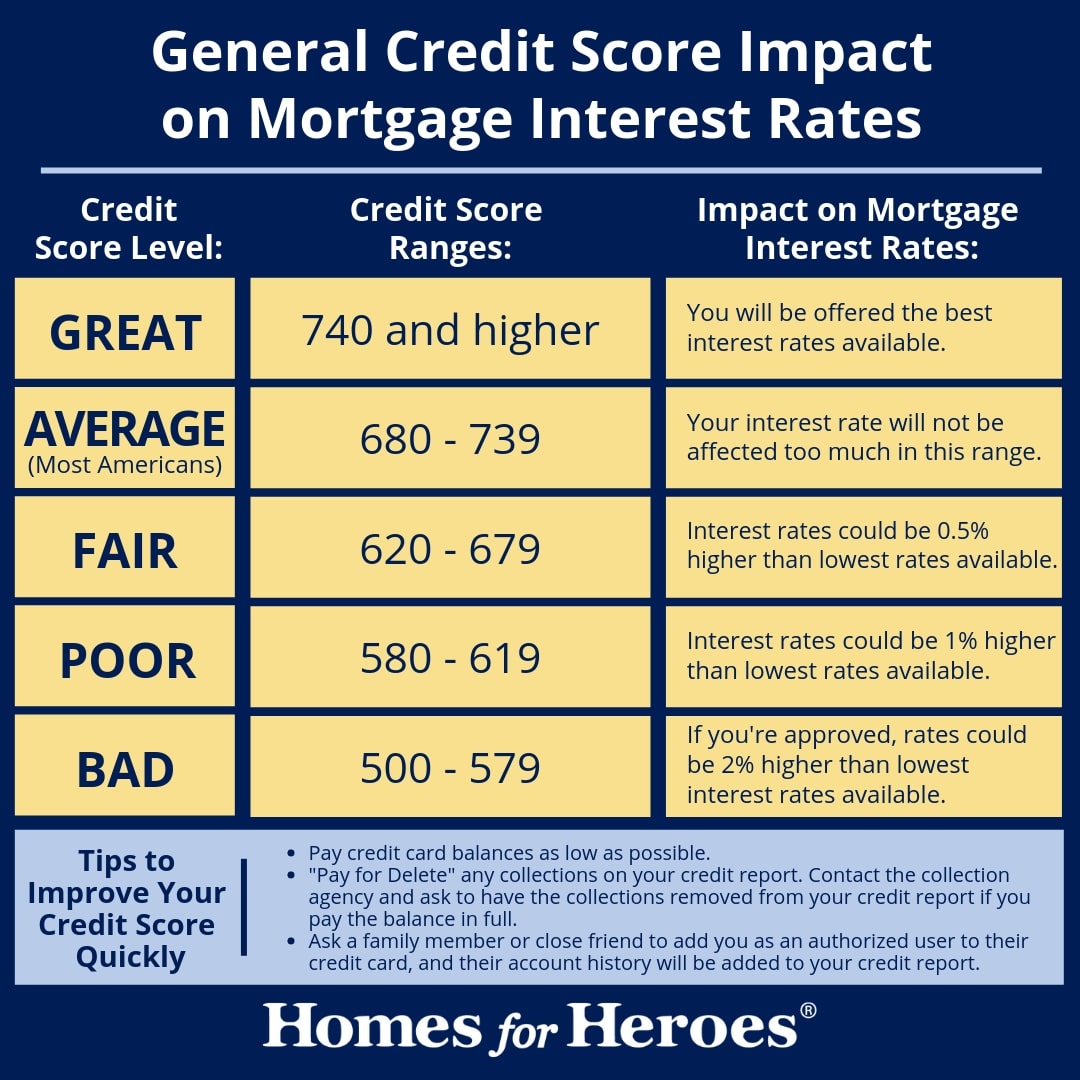

Also, if you’re looking to buy a house with a bankruptcy on your credit, you will need to wait at least 2 years before a lender will start considering you for a new mortgage. When it comes to the actual number, anything less than a 670 FICO® Score is considered “bad” or “subprime,” according to Experian™, one of the three main credit bureaus. More specifically, a fair score is 580 to 669, while a poor score is 300 to 579.

Additionally, different types of mortgages through the same lender may have varying credit score requirements. Various home loan programs can accept borrowers with no credit score, as long as you prove you’re financially responsible in other ways. This means you wouldn’t need to depend on a co-signer to get approved. But there are mortgage lenders who will accept loan applications with no credit history. Conventional mortgages, VA loans, and USDA loans may also be an option. However, the rules for these types of mortgages are a little stricter for borrowers with no credit history.

Make your payments on time

This effort helps increase your credit score because you will decrease your credit utilization, which is a huge factor in determining your score. Remember, it’s best to have a higher credit score to buy a house and apply for mortgages. Let’s check out some of the loan options available and the average credit score requirements for each of them. Your credit score tells a lender about your spending habits, payment reliability, and the likelihood of mortgage repayment. Low credit scores mean you’re a higher risk for a lender but do not have to mean your dream of owning a home has to come to an end. Down payment – There’s a reason why they say, “Cash is king.” When you have a low credit score, the more money you can put down, the better off you will be.

A score of 620 may be enough to land a conventional loan, especially if you have a high income or offer a down payment of 10% or more. If you're approved for a conventional mortgage with a fair credit score, you may end up with a higher interest rate than is currently advertised. Lenders look favorably on high credit scores because they indicate that you've done an excellent job managing credit in the past. Borrowers with high scores are offered the lowest interest rates and have the easiest time landing loans when they need them. If you don’t qualify for any government-backed programs, you can still get a conventional loan with bad credit. The FHA loan program is one of the most popular among first-time homebuyers.

Explore more mortgage articles

Of course, if you’re still more than a year out from buying a home, it’s a great idea to start building up credit. The stronger your credit score and report, the better deal you’ll get on your mortgage. You might be tempted to improve your low credit score by opening new credit cards, or even taking out a loan, before you apply for a mortgage. What this means for you is that not all lenders will do conventional loans with no credit score. And, in place of a traditional credit report, lenders may consider other financial obligations that typically don’t show up in your credit history. But lenders still need proof you’ll make good on your loan’s monthly payments.

All you need to do is make sure you make all payments on time and pay off your other debts. After you have increased your credit score, you may have the opportunity to refinance your home and obtain a lower interest rate and payment. First-time home buyers tend to have lower credit scores than the general population, and that’s okay. There are plenty of mortgage programs meant to help first-time buyers move into homeownership. There’s a large selection of mortgage loans geared toward first-time home buyers, and which allow for lower credit scores.

If you add many new accounts at around the same time, they will drop off your report together, and your score will bounce back. Only this time you will have better credit utilization, so your score will be higher. You can also use these accounts to add more to your credit history. If you need to increase the available credit to improve your utilization, applying for new accounts is an option.

When evaluating offers, please review the financial institution’s Terms and Conditions. If you find discrepancies with your credit score or information from your credit report, please contact TransUnion® directly. To see scores for mortgages, you can purchase a full report from myFICO.com. The most economical approach is to sign up, download the first month’s information, then cancel the service before the next billing cycle. Your social security number is not required to get started, and all quotes come with access to your live mortgage credit scores.

Get a mortgage pre-approval and gain access to your mortgage credit report. Whether your credit history is strong or weak, you’ll have a clear plan forward. For applicants without a score, the USDA accepts a "non-traditional tradeline." Typically, it asks to see 12 months' worth of proof that you've paid other bills on time.

There are population requirements to be able to use this type of loan. You can see the population guidelines on the USDA mortgage website. If you have a credit score that is lower than 670, you will be considered to have bad credit based on the FICO scale.

If you are in the process of buying a home and have recently fixed credit reporting errors, you can ask the credit bureaus for what is referred to as a rapid rescore. If you need a minimum credit score to buy a home and you’re just below it, the rapid rescore can help. When you apply for a traditional mortgage loan, the lender can set whatever minimum credit score they want. However, with most conventional mortgages, the acceptable credit score range will be similar. Depending on your credit score, you might still qualify for low credit score mortgage options—but you should expect to pay a higher interest rate, says Sheinin.

Many people who are interested in purchasing a house want to know the minimum credit score requirement. Another option that is gaining in popularity is the rise of rent to own home ownership programs. There are companies and investors that will purchase a property for you and lease it to you with an option to purchase it from them at a later date. This is a great alternative to traditional mortgage programs if you are having trouble getting approved. This program allows you to purchase a home if you are facing credit and down payment hurdles. Another military member benefit is access to the Navy Federal Credit Union’s 100 percent financing loan.

Here are some government-backed loan options if you have poor credit. A copy of your credit report – the lender will require a credit check and report. Since you have a low credit score, you’ll probably need to fit into a custom-tailored mortgage program to your needs. Having a good credit score will help you get a lower interest rate on a mortgage, access to better financing options, and avoid being denied altogether. If you have a lower credit score because you’ve consistently mismanaged debts in the past, a lender will be much less likely to approve you for a mortgage. Taking on new debt could limit your loan options in another way, too.

No comments:

Post a Comment